It seems that ever since Mitt Romney began running for President, the media has gained an increased interest on the estate planning techniques of the wealthy. As I have outlined before, one of Mitt Romney’s more successful techniques was the use of an intentionally defective grantor trust or IDGT. Another technique which is now getting quite a bit of media coverage is known as the Zeroed-Out GRAT or 2-Year Rolling GRAT. A GRAT is a grantor retained annuity trust that is established under the Internal Revenue Code. The GRAT rules were established by Congress in an effort to control certain abuses. However, they actually codified a technique that allowed for greater estate tax savings.

Under a GRAT, a grantor creates a trust and transfers property to the trust and retains an annuity payable for a term of years. At the end of the term, the trust property will go to the trust’s beneficiaries (either outright or in trust for their benefit). The initial transfer of property to the trust constitutes a gift for tax purposes which will eat up a person’s lifetime exemption amount. The value of the gift, however, is calculated based on actuarial tables based on the life of the grantor and based on interest rates published by the IRS (also known as the “hurdle rate”). Because of this, if assets transferred to the trust appreciate at a rate faster than the hurdle rate the grantor can transfer the excess appreciation, free of gift tax, to the grantor’s heirs. The major downside is that if the grantor dies before the GRAT terms expires, all trust assets are included in the grantor’s estate–thereby causing the grantor to lose the opportunity to do other estate planning that might have successfully removed the property from the estate.

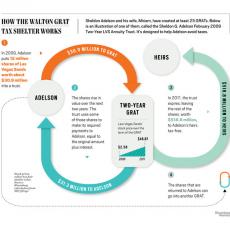

A Zeroed-Out GRAT comes into play when the value of what the grantor gets back in the form of the annuity (actually the present value of the annuity interest) is equal to the value of the property transferred. In this situation the grantor makes a large gift of property to the GRAT, but sets the annuity at an amount so that, for gift tax purposes, there will be nothing left to pass to the heirs at the end of the term. However, if the trust’s assets appreciate above the hurdle rate, there will be value and appreciation that will pass tax free to the children. By utilizing a Zeroed-Out GRAT, a grantor can pass large amounts of value to their children gift and estate tax free.

But what if the assets you own have a volatile value and there is no guarantee that over many years there will be a net amount of appreciation? In this case, one can utilize what is called a series of Zeroed-Out “rolling” GRATs. Generally, this entails establishing a series of consecutive 2-year GRATs. Because the terms are so short, it reduces the likelihood of dying during the term. In addition, if there is a down swing in value it will only affect the GRAT for the 2 year term. If there is a subsequent upswing in value that exceeds the hurdle rate the value can be passed on to the heirs. In a sense, it is a one way ratchet that will pass on value to heirs when the assets appreciate.

As with all estate planning techniques, one must consider their unique family circumstances, their assets, and current law to determine whether a GRAT makes sense.

The helpful info graphic above visually explains the use of the rolling GRAT technique, making references to billionaire Sheldon Adelson (via Bloomberg News).